In several recent engagements, Grayslake was tasked with evaluating the market-wide impact of a broad-reaching governmental policy change. This challenge is unique in that there are countless factors that must be taken into consideration when constructing a but-for world at the market level.

This stands in stark contrast to the relatively straightforward but-for world that is typical in real estate engagements. As an example: What rent would I have been able to achieve but-for a construction defect? Or perhaps: What would my interest rate have been but-for a three-month delay? The goal of any but-for exercise is to isolate the independent variable and create a defensible version of reality where the harmful act never happened.

So when Grayslake is asked to examine the impact of a specific policy on an entire market, isolating one single variable is more challenging. However, we have a deep, industry-based understanding that government and land-use policies heavily impact development patterns in a specific market. Often, litigators involved in disputes over government policies look to experts to frame how these policies impact their cases. We have found that in evaluating these policies, identifying existing natural experiments and case studies that have taken place in the real world is our most powerful tool.

What Kind of Policies Are We Discussing?

Governmental/policy changes is a broad category encompassing multiple potential issues. Consider the following examples, many of which were present in cases Grayslake has been engaged on the last 24 months:

- Downzoning / Upzoning: Density, height limits, FAR caps

- Historic preservation overlays

- Parking minimum reforms

- Affordable housing changes or set-asides

- Expansion or introduction of rent control / rent stabilization

- Eviction moratoria (like during COVID) or change in eviction laws

- Transfer taxes / mansion taxes

- Creation or dissolution of Tax Increment Financing or Opportunity Zones

- New environmental or building regulation (Electrification mandates, seismic retrofit, flood plan changes)

- Short-term rental bans/restrictions

It’s worth noting that all of these laws or policies can impact the development industry in either a positive or a negative way. In both cases, the impact needs to be quantified and defended with a rigorous analysis.

What Drives Investment and Development in a Market?

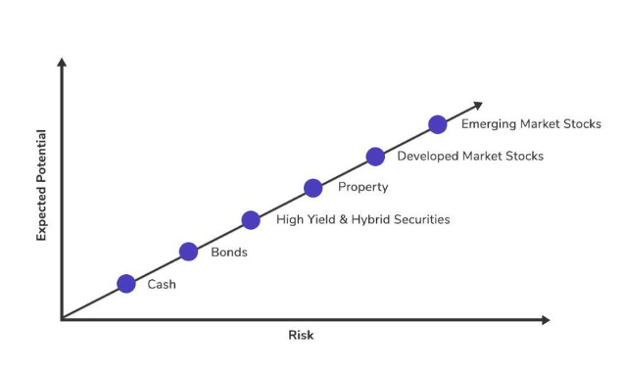

To fully address the policy impact issue at a city-wide or market-wide level, one must first understand the fundamentals of real estate investment and the capital markets that underlie their decision making. Real estate investors and developers compete for capital from lenders and investors that typically have many available capital allocation alternatives. In order to attract equity or debt capital, the expected returns from future cash flows must be commensurate with the perceived risks of that investment. This is commonly referred to as the risk-return profile spectrum, an example of which is shown below.

In the context of this risk-return spectrum, when the risk (or perceived risk) of an investment changes substantially, the expected return changes as well. At a city-wide level, the risk-profile can change when new policies or laws are enacted. This can then result in a significant shift in the ability to attract capital not only for new investors or developers, but for existing owners and operators as well. In turn, this impacts the demand for investment from capital providers in a specific jurisdiction and ultimately has a downstream impact on supply. This can be particularly pronounced in the multifamily housing market, as seen in our two examples below:

The Tale of Two (Twin) Cities:

On November 2nd, 2021, the city of St. Paul, Minnesota approved a new “Rent Stabilization Ordinance” capping annual rent increases at 3% for all multifamily rental properties, including new construction. The reaction from the investment and development community was overwhelmingly negative, with a major developer who had worked on developments in St. Paul for 30 years claiming “we, like everybody else, are re-evaluating what – if any – future business activity we’ll be doing in St. Paul.” Another builder with several major projects underway claimed “if our banking partners won’t loan us dollars to build the buildings that are planned as market rate because they can more safely lend their dollars elsewhere, we will not be able to build the market rate projects.”

Four months later in March of 2022, data compiled by the U.S. Department of Housing and Urban Development for the prior three months concluded multifamily building permits in St. Paul were down more than 80% compared to the same period during the previous year. Conversely, Minneapolis, the neighboring “twin-city” saw an increase in year-over-year permits.

In this specific situation, the creation of a but-for world to examine the impact of a new rent control ordinance was apparent in the actual world for the twin city. The perceived risk profile of St. Paul significantly shifted, which in turn shifted the investment expectations, and had a near-immediate impact on the appetite and supply for new development. The question of damage to investors can be seen in the “actual world” that played out in Minneapolis.

Notably, in 2025 the city of St. Paul overturned its rent control ordinance and voted to permanently exempt new construction and rentals built after 2004 from the ordinance. The decision was made “due to concerns about the impact on housing construction and development in the city.”

High Rises Across the River:

The nation’s capital, Washington D.C., has long been famous for its skyline, or lack thereof.

The city’s tallest structure is the Washington Monument, standing at 555 feet, which was completed in 1884 after nearly thirty years of construction. At the time, the Washington Monument was the tallest structure in the world, until being overtaken in 1889 by the Eiffel Tower. Rounding out the current top five tallest buildings in the D.C. is the National Basilica, the National Cathedral, the Old Post Office Pavilion, and the United States Capitol. These are the only five structures in the city with a height eclipsing 300 feet. None of these buildings are considered traditional skyscrapers, nor are they modern office buildings, residential buildings, or hotels. Surely as a major metropolitan area that serves as the nation’s capital, there is strong demand for vertical construction. As an example, New York City has 1,072 buildings over 300 feet tall. Significantly smaller cities by population and GDP such as Cincinnati, OH and Louisville, KY, for example, have 17 and 12 buildings over 300 feet tall, respectively.

So what is happening in DC? The short answer is regulation. In 1910, Congress passed the “Height of Buildings Act” that effectively limited building heights to 130 feet in Washington DC. This was driven by the city’s interest in preventing fire hazards and “preserving character.” Similar to the case with the Twin Cities, what is the proper way to analyze a potential but-for world for the entire market of Washington D.C.? How does this law impact demand for development and investment, and therefore owners and tenants in the city? In this case, the federal law has existed for more than a century, so it is not as simple as simply looking at the permit since its implementation, as we did in St. Paul. However, similar to Minnesota, simply looking across the river can be a very effective exercise.

Only a short walk across the Key Bridge spanning the Potomac River, Arlington, Virginia has forty buildings taller than 200 feet, fourteen of which are multifamily buildings built since 2020. This is an indication that the greater Washington D.C. metro has a large appetite for high-rise development, and it is simply the regulation that is prohibiting this development from happening in D.C. Below is a visual representation of multifamily buildings with more than 100 units in both Washington DC (white) and Arlington, VA (blue). The relative height of Arlington multifamily buildings is significantly greater than DC’s.