In commercial real estate, the lease functions as the engine that drives value. Rents traditionally reflect a wide range of factors, such as location, economic conditions, and interest rates. One factor, however, is routinely underappreciated by even the most sophisticated market participants: the financial strength of the entity signing the lease.

Our recent work compared the economics of leases held by uniquely high-credit tenants against those held by typical private-sector tenants. The distinction matters more than most people realize. Investment-grade tenants carry a degree of financial security that lower-credit businesses cannot replicate. That guarantee translates directly into a lower risk profile, and in real estate, lower risk means higher value. We found that tenant credit quality can swing property valuations by millions of dollars, even when the physical space, location, and rent remain identical.

The Economic Logic of Credit Quality

To understand why tenant credit quality moves valuations so significantly, start with how investors price income-producing real estate. At its foundation, a single-tenant net-leased property is a financial asset similar to a bond or an annuity. Its value is determined by the expected cash flows it will generate and the risk that those cash flows might not materialize. These two variables move in opposite directions: as risk decreases, value increases.

The primary source of risk in any leased property is the tenant. A tenant who fails to pay rent or goes bankrupt can quickly turn a stable income stream into a costly vacancy. Conversely, a tenant with strong financials makes future rent payments more predictable. Real estate investors will always pay a premium for this predictability. This premium is expressed through capitalization rates, or “cap rates,” which represent the ratio of a property’s annual net operating income to its market value. When investors perceive lower risk, they accept a lower return. Consequently, they pay a higher price for the same income. Tenant credit quality is not merely a qualitative factor; it serves as a direct input into property value.

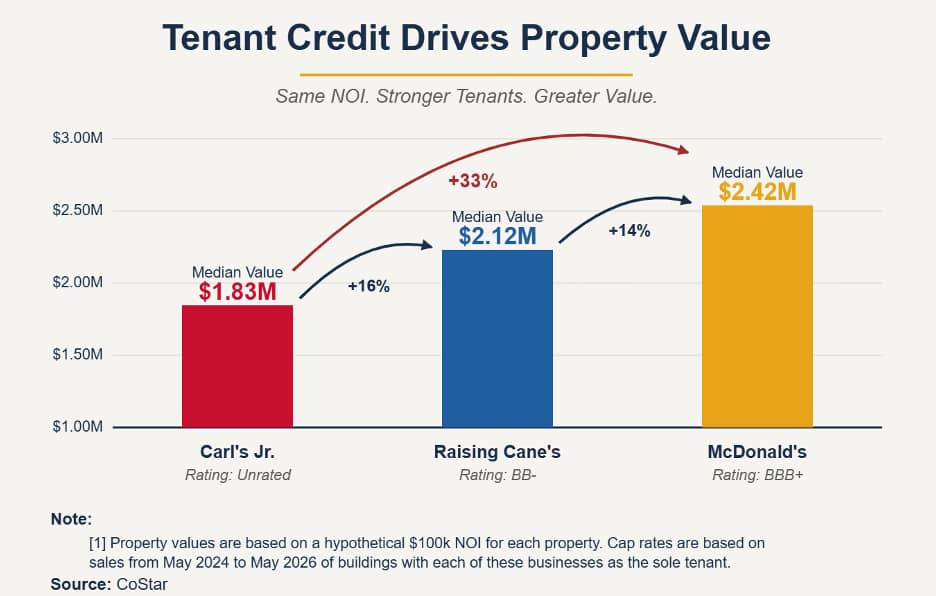

The Numbers Behind the Premium: A Case Study in Fast Food Tenants

To quantify the credit premium[NM5] , we analyzed single-tenant net-lease sales across three quick-service restaurant brands with meaningfully different credit profiles: McDonald’s (rated BBB+), Raising Cane’s (rated BB-), and Carl’s Jr. (unrated). The three brands occupy similar pad-site real estate, lease in similar markets, and sign broadly comparable lease structures. What sets them apart is the financial strength of the entity backing the rent check – making them a clean illustration of the credit premium in insolation.

Across our dataset of sales in the last two years, the results were clear. McDonald’s properties traded at a median cap rate of 4.13%, Raising Cane’s at 4.71%, and Carl’s Jr. at 5.48%. The table below illustrates the impact on property value, assuming an identical building producing $100,000 in annual net operating income.

| Tenant | Credit Profile | Median Cap Rate | Property Value[1] |

| McDonald’s | BBB+ | 4.13% | $2.42M |

| Raising Cane’s | BB- | 4.71% | $2.12M |

| Carl’s Jr. | Unrated | 5.48% | $1.83M |

The roughly $600,000 gap between the value of our hypothetical McDonald’s and Carl’s Jr. properties represents what the market charges for tenant credit risk. In this case study, the building is the same, the location is the same, and the rent is the same—only the signer on the lease has changed. Investors will pay 33% more when an investment-grade corporate guarantor like McDonald’s stands behind the cash flow rather than an unrated operating company (like Carl’s Jr.).

This pattern extends well beyond fast food restaurants and appears across every sector of real estate. The size of the credit premium varies, but the direction holds: stronger credit produces measurably higher property value on otherwise identical terms.

Beyond Valuation: Operational and Financing Advantages of High-Credit Tenants

The benefits of a high-credit tenant do not stop at property value. Landlords also enjoy meaningful operational and financing advantages.

On the operational side, these tenants can reduce management burdens significantly. They stay longer and require fewer concessions than typical private businesses. This difference is vital because tenant turnover is expensive. Vacancies trigger downtime rent loss, brokerage fees, and substantial allowances for tenant improvements. Our recent work found that a superior tenant’s higher renewal rate saves the landlord an average of $261k in vacancy and lease-up costs for a 20,000 square foot space leased at market rates.

On the financing side, landlords with investment-grade tenants may qualify for Credit Tenant Loan (CTL) financing. This specialized lending structure underwrites against the tenant’s credit rating rather than the real estate itself. CTL financing can unlock leverage exceeding 100% of the property’s value, which is a term unavailable to landlords with lower-credit occupants.

For all of these reasons, tenant credit shapes how a property is valued, operated, and financed. In legal disputes and litigation, all three dimensions are often underexamined and underappreciated because the focus is typically on rent, rather than on the entity paying it. The value tied to the guaranteeing entity is rarely small, and should be a determining factor in valuing commercial real estate.

Why Precise Analysis Matters

Capturing value requires more than a quick review of asking rents. Resolving complex real estate disputes demands a rigorous analysis of market benchmarks, submarket rent distributions, and the careful quantification of benefits that rarely appear on the face of a contract. Grayslake Advisors brings this level of clarity to opaque transactions. Whether a matter involves lease valuations or above-market rent claims, our work translates complex real estate concepts into defensible, evidence-backed conclusions for litigators and the courts.